An Orange County venture capital term sheet isn’t a final contract. Think of it as a handshake agreement on paper—a non-binding document that outlines the fundamental terms and conditions for an investment. For entrepreneurs, it’s the strategic blueprint for a future partnership with an investor, ensuring everyone is aligned before dedicating significant resources to drafting final legal agreements.

Securing this document is a major milestone in any Orange County startup’s fundraising journey. It’s the foundation for a healthy, long-term relationship and a critical step toward scaling your vision.

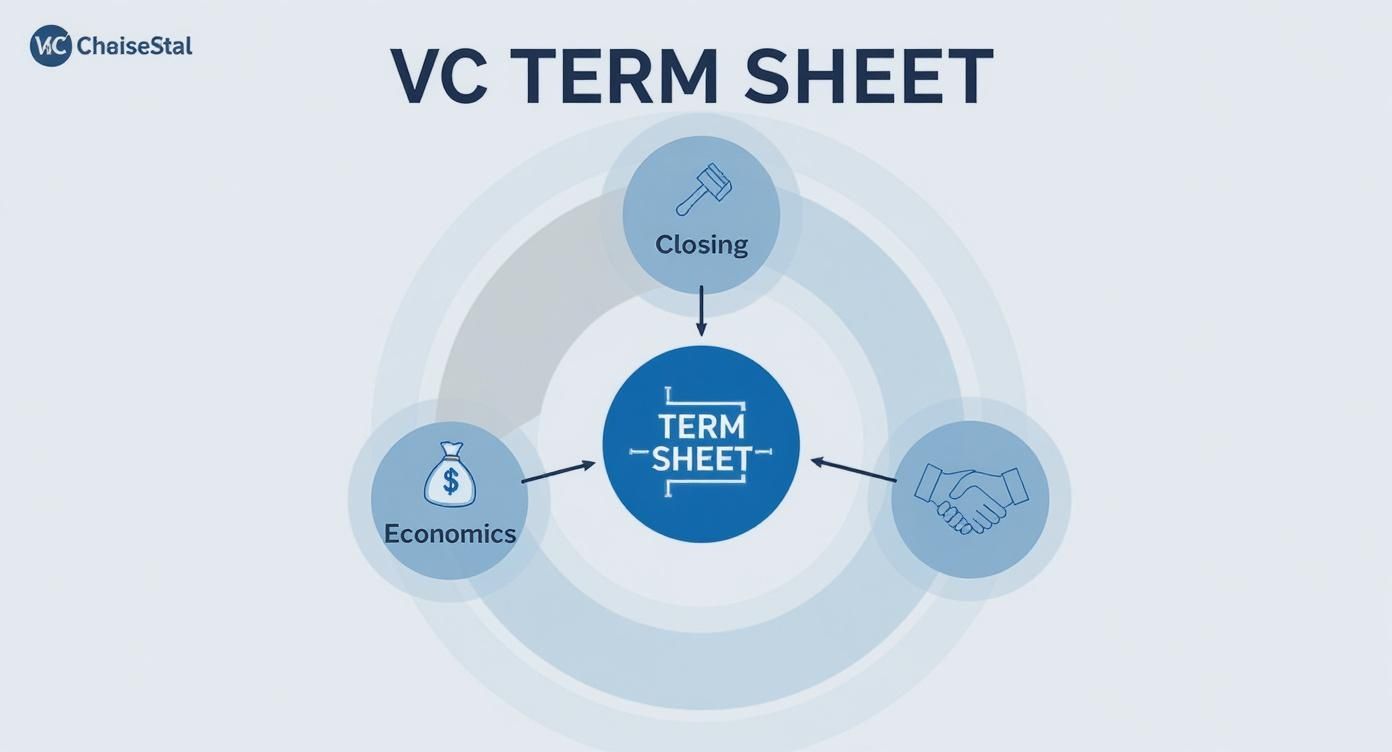

The Strategic Blueprint For Your Orange County Startup Investor Partnership

Receiving an Orange County venture capital term sheet is a powerful moment of validation. It signifies that an investor sees tangible potential in your startup and is serious about committing capital. But this is no time to relax; it's the start of the negotiation. The purpose of a term sheet is to align founders and investors on the deal's structure, preventing major misunderstandings down the road.

The terms laid out here will dictate everything from ownership percentages to how critical company decisions are made. These norms have been shaped by decades of deal-making. In fact, a foundational analysis of 1,528 financing rounds over ten years provided incredible insight into how these deal components function in the real world, and that data continues to inform VC practices. You can explore the research on historical term sheet trends to see how these structures have evolved.

To master a venture capital term sheet, it helps to break it down into three core areas:

- The Economics: This is the financial core of the deal. It covers your startup's valuation, the investment amount, and the mechanics of how proceeds are distributed at a liquidity event (like an acquisition). These terms directly impact the financial outcome for founders, the team, and investors.

- Control and Governance: This section defines the balance of power. It specifies who sits on the board of directors, what voting rights investors hold, and which strategic decisions—like selling the company—require their approval.

- The Path to Closing: This is a procedural roadmap. It lists the conditions precedent to closing the deal, such as the successful completion of due diligence, and establishes a timeline for executing final legal agreements.

An Orange County venture capital term sheet is where the theoretical value of your startup meets the practical reality of a financial partnership. Founder excellence means focusing as much on control and governance as you do on the headline valuation.

At its heart, an Orange County venture capital term sheet is a tool for alignment. It forces an open conversation about expectations, roles, and the long-term vision. A well-negotiated term sheet does more than secure funding for early-stage companies; it builds a solid foundation for a partnership that can withstand the pressures of scaling a startup. It ensures that when you finally sign the definitive agreements, you and your new investors are truly ready to build together.

The Economic Terms That Define Your Payout

Let’s dissect the financial engine of your Orange County venture capital term sheet: the economic terms. These clauses extend far beyond the headline valuation; they establish the rules that determine who gets paid, how much, and when. Mastering these concepts is non-negotiable for founders, as they directly shape the financial future for you, your team, and your investors.

This is where your fundraising strategy meets financial reality.

As you can see, the economics, control, and closing mechanics are interconnected. They are the three pillars supporting the entire investment agreement, ensuring all parties are aligned before capital is transferred.

Valuation: The Starting Point of Your Deal

Valuation is the first number everyone focuses on, but it comprises two distinct figures: pre-money valuation and post-money valuation.

The pre-money valuation is the agreed-upon value of your startup before the new investment. The post-money valuation is the value of the company immediately after the investment.

The formula is simple:

Pre-Money Valuation + Investment Amount = Post-Money Valuation

For example, if an investor offers $2 million at an $8 million pre-money valuation, your post-money valuation is $10 million. This calculation is critical because it determines the price per share. In this scenario, the investor’s $2 million buys them 20% of the company ($2M ÷ $10M).

Liquidation Preferences: Who Gets Paid First

This is arguably the most critical economic clause in a venture capital term sheet. A liquidation preference dictates who gets their money back first in a liquidity event, such as a sale of the company. It serves as the investor’s downside protection.

Think of it as the investor's "first-out" guarantee.

- 1x Non-Participating Preference: This is the standard, most founder-friendly structure. Investors have a choice: either receive their original investment back (1x their money) OR convert their preferred stock into common stock to share in the proceeds pro-rata. They will choose whichever option yields a higher return.

- Participating Preference: This term is significantly more investor-favorable. Investors receive their money back first (the preference), AND then they also receive their pro-rata ownership share of the remaining proceeds (the participation). A "2x participating" preference is even more aggressive—they get double their money back before founders see a dollar, plus their share of the rest.

A high valuation feels like a win, but an aggressive liquidation preference can eliminate founder returns in a modest exit. Always model the payout scenarios at different sale prices to understand the true impact of this term.

The Option Pool Shuffle and Its Impact on Dilution

Before closing, VCs will almost always require you to create or increase your employee stock option pool (ESOP). This is a block of equity reserved to attract and retain future talent—a best practice for hiring and team building.

The critical detail, however, is when this pool is created.

Investors will insist the option pool be created from the pre-money valuation. This means the dilution from these new options impacts existing shareholders—namely, you and your early team. For instance, creating a 10% option pool on an $8 million pre-money valuation effectively reduces your valuation to $7.2 million before the new investment is even made. Understanding these investor trends driving startup valuations is key to anticipating these negotiation points.

Anti-Dilution Provisions: Protecting Investor Stakes

Finally, anti-dilution provisions act as an investor's insurance policy against a "down round"—a future financing round at a lower valuation. These clauses adjust the investor's stock conversion price, granting them more shares to protect the value of their original investment.

In today's market, this is a practical concern. As reported by Carta for Q3 2024, of the $20.1 billion raised by startups on its platform, over 20% of rounds were down rounds. This kind of valuation reset highlights why investors prioritize protective terms like anti-dilution. As a founder, understanding these mechanics is crucial, as they can significantly alter your ownership in a challenging fundraising environment.

Understanding The Control Terms VCs Require

It's easy to fixate on valuation, but a venture capital term sheet is a tale of two parts: economics and control. While economics sets the price, control terms dictate who makes the decisions. When you accept venture capital, you are not just selling equity; you are bringing a new partner into your company's governance structure.

These clauses are about power and define how much decision-making authority you retain and how much you share. Getting these right is fundamental to steering your company's future and building a healthy, aligned relationship with your investors.

This part of the term sheet covers everything from board composition to special investor veto rights. Think of it as the constitution for your newly funded startup.

The Board Of Directors: Your Company's Command Center

The most direct way an investor influences your startup’s trajectory is by taking a seat on your Board of Directors. This body holds ultimate authority on major strategic decisions, from hiring or firing a CEO to approving annual budgets and authorizing a pivot.

A typical early-stage board includes:

- Founder Seats: One or two seats are typically reserved for the founding team.

- Investor Seats: The lead investor will always require a dedicated seat.

- Independent Seats: An outside expert with relevant industry experience who provides a neutral perspective.

For a seed or Series A startup, a three or five-person board is common. A three-person structure (one founder, one investor, one independent) often feels balanced. However, a five-person board with two investor seats can shift the balance of power away from the founders. The composition outlined in the term sheet is paramount.

Protective Provisions: The Investor's Veto Power

While the board handles high-level governance, protective provisions give your investors a direct veto over a specific list of critical corporate actions. Think of them as an "emergency brake" investors can use if they believe the company is heading toward a value-destroying decision.

These provisions mean the company cannot proceed with certain actions without approval from a majority of the preferred stockholders (your investors). Common items on this list include:

- Selling the company or executing a merger.

- Issuing new stock that dilutes investors, particularly shares with senior rights.

- Incurring significant debt.

- Changing the size or composition of the board.

- Authorizing a dividend.

These provisions are not about micromanagement. They are a standard and reasonable tool for VCs to protect their capital from catastrophic decisions. The negotiation focuses on ensuring this list is standard and doesn't impede day-to-day business operations.

It’s also important to recognize that the market for these terms shifts. In uncertain economic climates, investors become more focused on downside protection. For example, with early-stage financing sizes shrinking by 23% in 2023 and down rounds comprising 21% of deals in recent Q2 2025 data, investors are more focused than ever on protective measures. This climate makes it crucial for founders to know which terms are standard and which are overly aggressive. The full 2024 WilmerHale VC report offers an excellent analysis of these trends.

Drag-Along and Pro-Rata Rights

Two other technical-sounding terms with significant real-world impact are drag-along rights and pro-rata rights.

A drag-along agreement empowers the majority shareholders (which almost always includes the lead investor) to force minority shareholders—including founders—to sell their shares in an acquisition. While this may feel coercive, its purpose is to prevent a small number of holdouts from killing a deal that benefits the majority. It is a standard term that facilitates a clean exit.

Conversely, pro-rata rights are a major benefit for your investors. This clause gives them the right (but not the obligation) to participate in future funding rounds to maintain their ownership percentage. If your VC owns 20% of the company, pro-rata rights allow them to purchase 20% of the next financing round, preventing dilution of their stake. For VCs, this is how they increase their investment in their winning portfolio companies, and they value this right highly.

Navigating these control terms requires a clear understanding of where to stand firm and where to compromise. The table below outlines what "founder friendly" and "investor friendly" positions look like.

Founder Friendly vs Investor Friendly Terms

| Term | Founder Friendly Position | Investor Friendly Position |

|---|---|---|

| Board Composition | Founders control a majority of board seats (e.g., 2 founders, 1 investor). | Investors control a majority or have equal representation with an independent tie-breaker they approve. |

| Protective Provisions | A limited list of vetoes focused on major events like a company sale or issuing senior stock. | An extensive list of vetoes covering operational decisions like annual budgets, key hires, and debt. |

| Drag-Along Rights | High threshold for activation (e.g., requires >75% shareholder approval, including founders). | Low threshold for activation (e.g., requires only a simple majority of preferred stock). |

| Pro-Rata Rights | Limited or no pro-rata rights granted, giving the company more flexibility in future rounds. | Full pro-rata rights, and potentially "super pro-rata" (the right to buy more than their share). |

Remember, a term sheet negotiation is not a battle to be won but a partnership to be built. Your goal is to achieve a fair balance that protects your investors while preserving the operational freedom you need to build a category-defining company.

Spotting Red Flags and Navigating Key Clauses

After wrestling with the major economic and control terms, it’s tempting to think you’re done. However, a venture capital term sheet contains other clauses that can significantly impact your company’s future, your role within it, and your eventual financial outcome.

These clauses establish the ground rules for your partnership, setting expectations and aligning incentives for the startup journey ahead. Learning to spot terms that are off-market or overly aggressive is more than a negotiation tactic; it’s an early indicator of your investor's character. An investor who pushes for one-sided terms from day one may reveal how they will behave when challenges arise.

Founder Vesting: The Golden Handcuffs

Investors are not just buying a piece of an idea; they are betting on the founding team's commitment to execute it. Founder vesting is the mechanism that ensures you remain dedicated to the mission. It means that while you own your shares on paper, you must earn them over time.

The industry standard is a four-year vesting schedule with a one-year cliff. Here's how it works:

- The Cliff: For the first 12 months, none of your shares vest. If you leave the company before your one-year anniversary, you forfeit all your equity. This is a standard protective measure for the company and its investors.

- Vesting: On your one-year anniversary, 25% of your shares vest instantly. The remaining shares typically vest in equal monthly or quarterly installments over the next three years.

This structure protects all stakeholders. It prevents a founder from leaving prematurely with a large equity stake, which would create a "dead equity" problem on the cap table and hinder future fundraising.

Single-Trigger vs. Double-Trigger Acceleration

What happens to your unvested stock if the company is acquired? This is governed by acceleration clauses, and the details are critical.

- Single-Trigger Acceleration: This means all your unvested shares vest immediately upon a change of control (the acquisition is the "single trigger"). This is extremely founder-friendly and therefore rare.

- Double-Trigger Acceleration: This is the market standard. Your shares accelerate only if two events occur: the company is acquired, and you are terminated without cause or resign for "good reason" afterward (the acquisition and termination are the "double triggers"). This structure incentivizes the acquiring company to retain the founding team.

The No-Shop Agreement: A Brief Engagement

Once you sign a term sheet, the investor needs assurance that you are serious. They are about to invest significant time and money in due diligence and do not want you to use their offer as leverage to solicit competing bids. This is the purpose of the no-shop clause (or exclusivity agreement).

The no-shop clause is one of the few legally binding parts of a venture capital term sheet. It requires you to cease fundraising conversations with other investors for a specific period. A fair timeline is typically 30 to 45 days. An investor request for 60 or 90 days is a red flag, as it could stall your momentum for months if the deal fails to close.

Knowing a Bad Deal When You See One

A fair term sheet should reflect current market standards. When you encounter terms that are wildly out of line, it often signals either an inexperienced investor or one attempting to gain an unfair advantage.

Here are a few major red flags to watch for:

- High Liquidation Preference Multiples: Anything above a 1x preference is a serious warning. A 2x or 3x multiple means investors receive two or three times their money back before founders and employees see anything. In most exit scenarios, this could wipe out the common stockholders entirely.

- Participating Preferred Stock: As mentioned earlier, this "double-dipping" right is heavily skewed toward the investor and has become rare in competitive financing environments. If an investor insists on this, you must understand its massive economic impact and negotiate firmly against it.

- Full-Ratchet Anti-Dilution: This is the most punitive form of anti-dilution. In a down round, it re-prices all of the early investor’s shares to the new, lower price, causing catastrophic dilution for founders and employees. Broad-based weighted average anti-dilution is the standard for a reason; full-ratchet signals a partner who is not aligned with the team.

Identifying these terms is not just about protecting your cap table; it’s about choosing a partner with whom you can build a business for the next decade. That relationship must start on a foundation of fairness, trust, and mutual respect.

Your Strategic Framework For Term Sheet Negotiation

Receiving a venture capital term sheet is a significant achievement in your startup growth journey. Take a moment to celebrate. Then, prepare for the next phase, because this is where your partnership truly begins to form. Negotiation is not about winning a battle; it's about methodically building the foundation for a durable, long-term relationship. Your objective is a fair deal that keeps all parties motivated and positions the company for success.

Your most powerful negotiating tool is established long before you reach the table: a strong set of alternatives.

Know Your BATNA: Your Strongest Leverage

BATNA stands for Best Alternative to a Negotiated Agreement, a concept core to effective negotiation. Simply put: what is your plan if this deal falls through? The stronger your alternatives, the more leverage you bring to the discussion.

An excellent BATNA could be a competing term sheet from another VC, a solid commitment from angel investors, or even a credible plan to bootstrap the company for another six to twelve months. When you have viable options, you are negotiating from a position of strength, not desperation.

Prioritize What Truly Matters

You will not win every point in a negotiation—nor should you try. Before responding with a redline, sit down with your co-founders and categorize every clause into one of three buckets:

- Must-Haves: These are your non-negotiable deal-breakers. This might include maintaining founder control of the board or securing a clean 1x non-participating liquidation preference.

- Nice-to-Haves: These are points you would like to win but will not derail the deal over, such as more favorable founder vesting acceleration or a slightly smaller ESOP.

- Giveaways: These are standard, investor-friendly terms you are prepared to concede. Agreeing to these demonstrates that you are a reasonable partner and helps focus the negotiation on your priorities.

Successful negotiation is an exercise in trade-offs. By knowing your priorities, you can strategically concede on less critical points to secure your must-haves, proving you are a thoughtful and strategic leader.

This framework empowers you to steer the conversation toward the terms that will genuinely shape your startup’s future.

Frame Requests Around Mutual Success

How you ask is as important as what you ask for. Avoid confrontational language. Frame your counter-proposals not as demands but as collaborative solutions for building a more valuable company together.

For example, instead of stating, "We reject this board structure," try this approach: "To preserve the agility that has driven our success, we believe a three-person board—including an independent member we mutually select—will enable us to execute faster and create more value for all shareholders."

This collaborative framing reinforces that you and the investor are on the same team, aligned toward a massive outcome. This is a critical opportunity to show investors what venture capitalists look for beyond the pitch deck—they are betting on founders they can build with.

Your Lawyer Is Your Strategic Advisor

Never negotiate a venture capital term sheet without an experienced startup lawyer. Their role is not just to interpret legal jargon but to provide vital market intelligence. They have seen hundreds of deals and know what is standard, what is aggressive, and what is a red flag.

A great startup lawyer acts as your strategic counsel. They can model the economic impact of different terms, advise on which battles are worth fighting, and serve as an essential buffer between you and the investors. Their fee is a small price to pay for a fair deal that protects your company, your team, and your future. It is a critical investment in building a powerful alliance.

From Term Sheet to Closing the Deal

Signing the venture capital term sheet is a celebratory moment, but it's not the finish line. It’s the starting signal for the final phase of the fundraising process, where your non-binding agreement is transformed into a legally binding partnership.

Once the term sheet is signed and the exclusivity period begins, the investor’s team initiates due diligence. This is not a casual review; it is a deep, formal investigation into every aspect of your startup.

The Due Diligence Gauntlet

Investors use due diligence to verify the assumptions they made about your business. This process is less about discovering new positive attributes and more about ensuring there are no hidden liabilities. For the VC, this is a critical risk management step. You can get a deeper look at what to expect in our guides on venture capital due-diligence.

Key areas of review include:

- Financials: A thorough analysis of historical financial statements, financial projections, burn rate, and unit economics.

- Legal: Scrutiny of corporate formation documents, cap table, intellectual property ownership, and key contracts.

- Team: Background checks on founders and key personnel.

- Technology: For tech startups, a technical audit of the product, source code, and systems architecture.

Think of due diligence as a comprehensive health checkup for your startup. The most effective way to accelerate this process and build investor trust is to have a well-organized virtual data room prepared in advance.

From Blueprint to Binding Agreements

While due diligence is underway, lawyers for both sides work to translate the high-level points from the term sheet into definitive legal documents.

The primary documents typically include:

- Stock Purchase Agreement: The formal contract for the sale of equity to investors.

- Investors’ Rights Agreement: Details key rights such as information access and pro-rata rights for future rounds.

- Voting Agreement: Outlines the board of directors' structure and shareholder voting arrangements.

This stage can take 30 to 60 days. Delays are common and often arise from negotiations over specific legal language or, more seriously, from red flags discovered during due diligence.

Finally, you reach the closing. This is the official event where all documents are signed and the investor wires funds to your company’s bank account. It’s a monumental milestone that marks the true beginning of your new partnership and the successful conclusion of a demanding fundraising process.

Common Questions About VC Term Sheets

The first time a founder encounters a venture capital term sheet, it can feel like learning a new language. Here are answers to some of the most common questions from entrepreneurs navigating this critical process.

Is This Thing Actually Binding?

For the most part, a term sheet is not legally binding. It functions as a letter of intent—a roadmap to ensure alignment before engaging lawyers to draft definitive deal documents.

However, two clauses are almost always binding and must be treated as such:

- The "No-Shop" Clause: This is your commitment to cease conversations with other investors for a specified period while you work to close the deal.

- The Confidentiality Clause: This is a mutual agreement between you and the investor to keep the details of your discussions private.

While you can technically walk away from the non-binding parts, doing so without a substantial reason can damage your reputation in the close-knit VC community.

Okay, We Signed. How Long Until the Money Is in the Bank?

After a term sheet is signed, you can generally expect the funds to be wired within 30 to 60 days. This period is dedicated to due diligence and legal documentation.

The investor's team will conduct a thorough review of your business—finance, technology, legal, and team—while lawyers on both sides draft and negotiate hundreds of pages of final agreements.

A well-organized data room and clean corporate records can expedite this timeline. Delays typically occur when diligence uncovers unexpected issues or when legal negotiations become protracted.

The biggest mistake founders make? Getting fixated on the valuation number. A sky-high valuation can be completely wiped out by aggressive terms like a hefty liquidation preference or punishing anti-dilution clauses.

Do I Really Need to Hire a Lawyer for This?

Yes, absolutely. Attempting to navigate a VC financing without an experienced startup lawyer is one of the costliest mistakes a founder can make.

A great attorney provides more than legal interpretation; they are your guide to what is "market" and what is off-market. Having seen hundreds of deals, they can identify when an investor is pushing for overly aggressive terms. They advocate for your interests and ensure you build your company on a solid legal foundation. View their fee not as a cost, but as a critical investment in your startup's future.

At Spotlight on Startups, we provide the clarity, inspiration, and authority you need to move forward with confidence. From deep dives into funding pathways to expert insights on what investors truly value, we deliver actionable knowledge for founders and investors. Learn more about building your startup.